1xBet Apk

| Name | 1xBet |

| Penyedia | XCorp N.V. |

| 3.6 K Ratings | 4.8 / 5.0  |

| Versi Terbaru | 2026 (v.23.12.0) (Last Update: Jan 2026) |

| Kesesuaian | Android 6.0+ / iOS 12.0+ |

Terms and conditions 18+

Pernah merasa repot buka situs taruhan dari browser setiap kali mau pasang taruhan? Nah, 1xBet app dibuat khusus supaya semua terasa lebih cepat, simpel, dan aman langsung dari genggaman. Di sini, kamu bakal tahu cara 1xBet app download, 1xbet download, instalasi di Android, update ke versi terbaru, dan cara mendapatkan 1xbet apk resmi, serta fitur menarik yang bikin banyak pemain Indonesia betah pakai aplikasi ini setiap hari.

Persyaratan Sistem untuk 1xBet Application

Persyaratan Sistem 1xBet App untuk Android

| Komponen | Spesifikasi Minimum | Rekomendasi untuk Performa Maksimal |

| Versi OS | Android 4.1 atau lebih baru | Android 8.0 ke atas |

| Ruang Penyimpanan | 60 MB ruang kosong di memori internal | 200 MB atau lebih untuk update dan data tambahan |

| RAM | Minimal 1 GB | 2 GB atau lebih untuk pengalaman lancar |

| Prosesor (CPU) | Dual-core | Quad-core atau lebih tinggi |

| Koneksi Internet | Stabil (WiFi atau data seluler) | WiFi cepat atau 4G/5G untuk live betting |

| Resolusi Layar | 800×480 piksel | 1280×720 piksel atau lebih tinggi |

| Izin Sistem | Aktifkan “Sumber Tidak Dikenal” sebelum instalasi | Tetap aktifkan untuk update manual aplikasi |

Cara Download 1xBet App untuk Android

Berbeda dengan aplikasi biasa, proses 1xbet download dan 1xBet app download for android memang butuh langkah ekstra. File 1xbet apk harus diunduh langsung karena memang tidak tersedia di Google Play Store.

Langkah-langkah 1xBet app download for Android secara manual (APK file)

- Pilih tombol “Unduh aplikasi 1xBet“

- File APK bakal otomatis tersimpan

- Tunggu sampai unduhan selesai – biasanya cuma beberapa detik

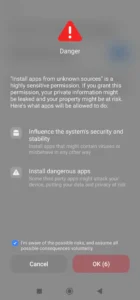

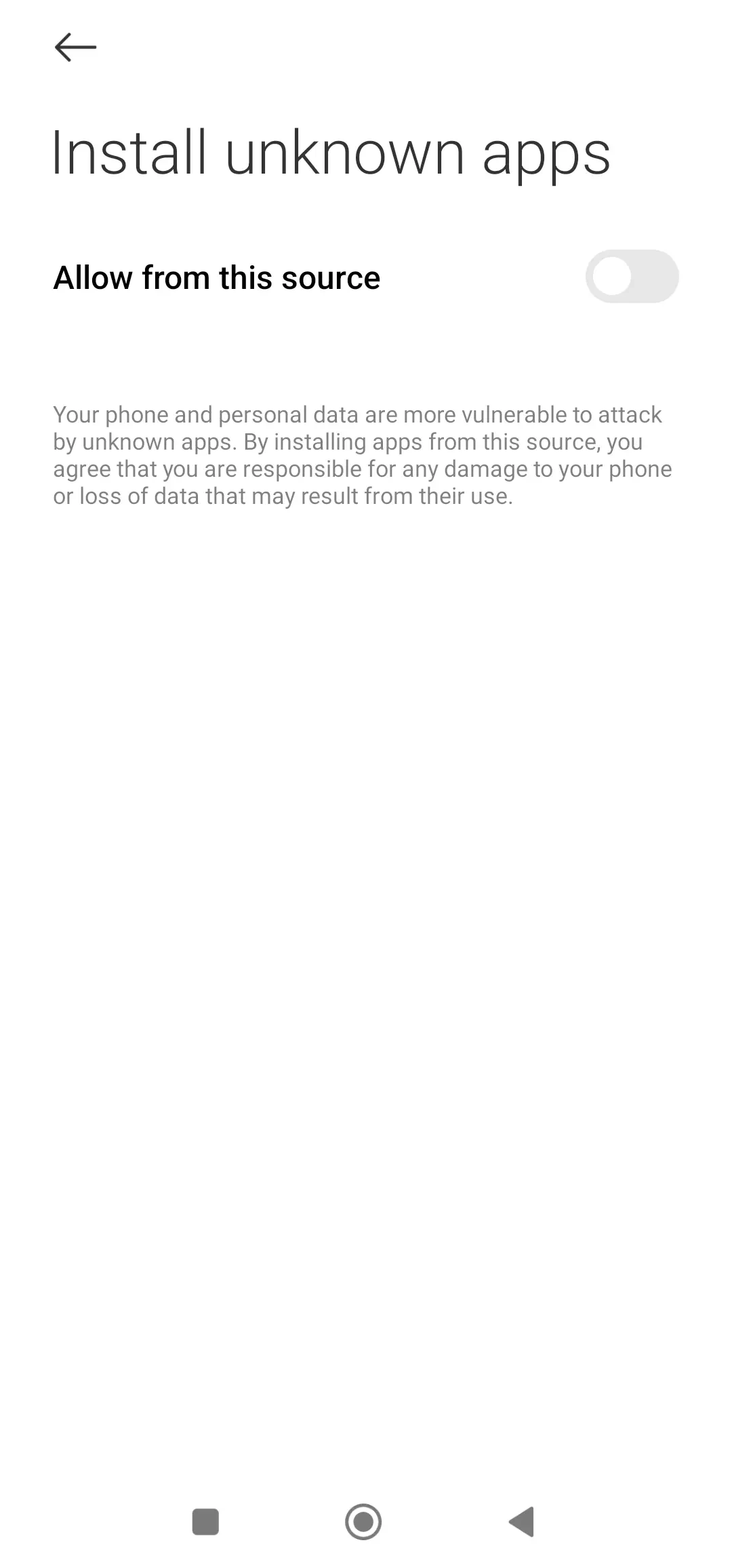

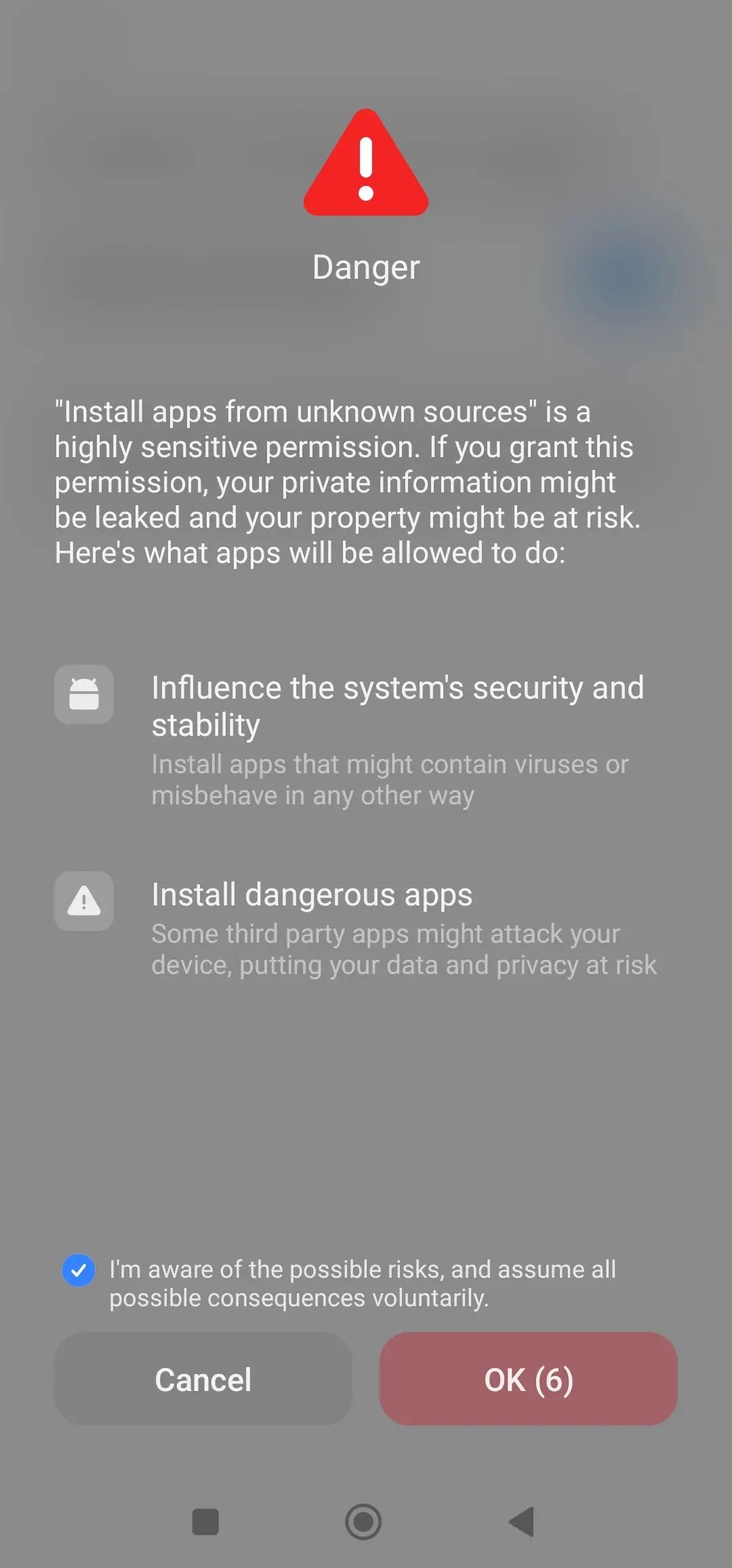

Mengaktifkan izin “Sumber Tidak Dikenal” sebelum instalasi

Masuk ke Settings > Keamanan, lalu aktifkan “Sumber Tidak Dikenal”. Tanpa langkah ini, sistem bisa menolak file 1xBet app android yang kamu unduh.

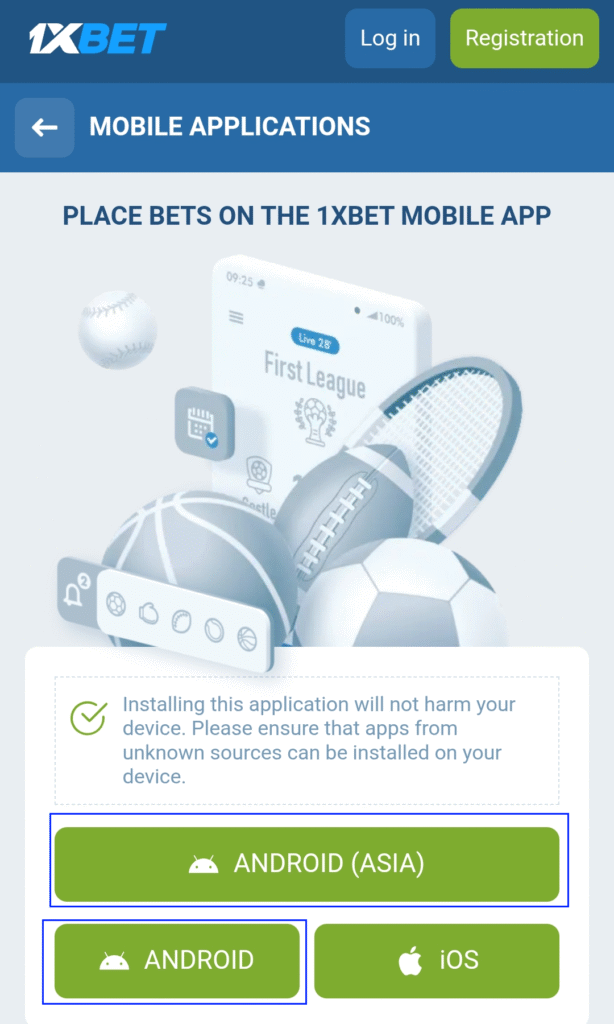

Langsung Download 1xBet App dari Situs Resmi

Cara paling cepat buat 1xBet app download atau 1xbet download? Yaitu langsung aja kunjungi situs resminya lewat link yang tersedia. Nanti kamu bakal otomatis diarahin ke halaman download khusus.

Buat yang pake HP Android, caranya gampang banget. Cari aja tombol yang bertuliskan “Android (ASIA)” atau “Android”, terus tekan tombol tersebut.

Dengan sekali klik, proses download 1xbet apk bakal langsung dimulai. Gampang kan? Ga pake ribet!

Proses Instalasi dan Membuat Akun Baru

Abis proses download selesai, sekarang saatnya install! Pertama, buka folder “Downloads” di HP-mu. Cari file APK yang barusan kamu unduh, lalu tap sekali aja untuk mulai instalasi.

Nanti bakal muncul layar yang kasih tau izin apa aja yang dibutuhin aplikasinya. Tenang aja, ini normal. Tinggal tekan “Install” dan tunggu prosesnya selesai biasanya cuma 30-60 detik kok.

Selesai install? Icon aplikasi bakal muncul di layar HP-mu. Tinggal buka, pilih “Daftar”, dan kamu bisa bikin akun pake nomor HP, email, atau one-click registration. Gampang banget, kan? Dalam beberapa menit, akunmu udah siap dipake!

Solusi jika file APK gagal diinstal

Aduh, aplikasi gagal instal? Jangan panik dulu. Biasanya sih ini karena memori HP udah penuh.

- Coba cek storage-mu, hapus file atau aplikasi yang jarang dipake buat ngasi ruang.

- Jangan lupa cek juga settingan “Sumber Tidak Dikenal” di security options. Udah diaktifin belum? Kalo belum, ya wajar kalo gagal.

- Bisa juga nih file APK-nya yang rusak, biasanya karena internet putus pas 1xbet download. Solusinya? Download ulang aja dari website resminya atau ulangi download 1xbet apk.

- Sebelum install ulang, coba restart dulu HP-mu. Sering banget lho cara sederhana ini berhasil.

- Terakhir, kalo pake antivirus, coba nonaktifin sementara. Kadang mereka suka ngeblok instalasi aplikasi dari luar Play Store.

Panduan 1xBet App Update

Cara Update Otomatis untuk Pengguna Android

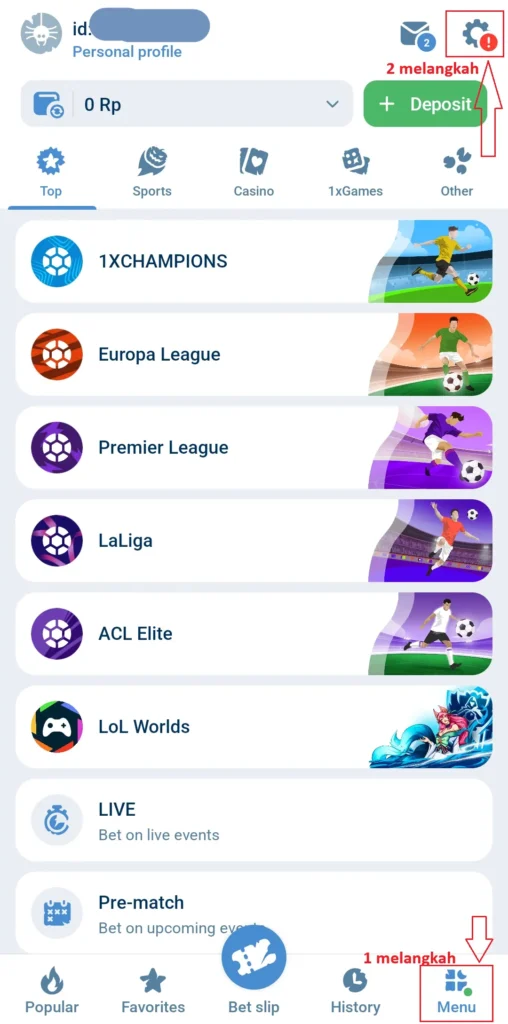

Biar aplikasi selalu up-to-date, caranya gampang banget. Pertama, buka dulu app yang udah terinstall di HP-mu. Trus, cari aja icon setting (biasanya gambar gir) yang ada di pojok layar.

Nanti di dalam menu settings, kamu tinggal cari opsi “Update” atau “Update Aplikasi”. Kalo nemu fitur auto-update, langsung aktifin aja. Dengan begini, aplikasi bakal otomatis ngecek versi terbaru setiap kali kamu konek ke WiFi.

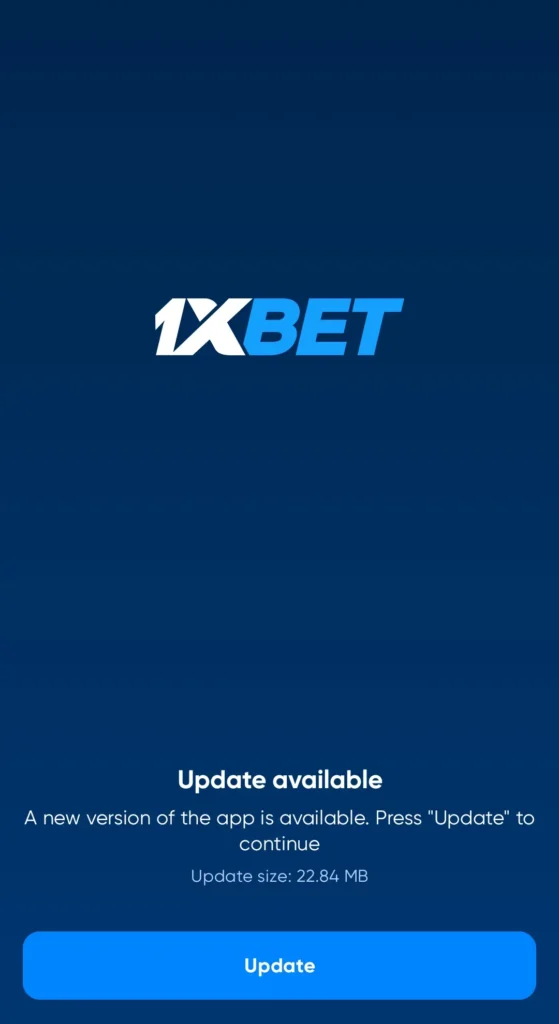

Begitu ada update tersedia, notifikasi bakal muncul sendiri. Tinggal klik “Download”, dan proses updatenya bakal jalan dengan lancar. Gampang kan? Nggak sampe 2 menit selesai!

Panduan untuk memperbarui aplikasi 1xBet secara manual

Kalau aplikasi nggak update otomatis, jangan khawatir. Kamu bisa kok update manual dengan gampang. Pertama, kunjungi lagi situs resmi lewat browser dan lakukan 1xbet download untuk versi terbarunya – persis kayak pas pertama kali install.

File 1xbet apk yang baru ini bakal timpa versi lamanya tanpa hapus data akun atau history taruhanmu. Begitu file selesai diunduh, tinggal dibuka. Sistem bakal tahu kalo ini update dan nampilin opsi “Update”.

Tekan aja tombol “Update” tersebut, dan versi terbarunya bakal terinstall. Tenang aja, semua data login dan informasi akunmu bakal aman terus kok setelah proses selesai. Gampang banget, kan?

Mengapa Penting untuk Selalu Melakukan 1xBet App Update?

Jangan malas update aplikasi, bro! Soalnya versi lama rentan banget error dan sering putus koneksi pas lagi seru-serunya live betting. Dengan update terbaru, aplikasinya jadi lebih ringan dan lancar tanpa lag.

Nih alasan lain kenapa kamu harus rajin update:

- Keamanan tambahan: Setiap update bawa perbaikan sistem keamanan buat lindungin data dan transaksi finansial kamu.

- Fitur baru: Sering banget tambah metode pembayaran lokal yang lebih praktis buat kita di Indonesia.

- Perbaikan bug: Masalah-masalah kecil yang bikin jengkel biasanya udah dibenerin di versi terbaru.

Buat kita di sini, update itu berarti kemudahan-seperti tambahan opsi deposit yang lebih familiar dan gampang dipake!

Cara Login dan Registrasi di 1xBet Mobile App

Kemudahan akses ke akun adalah salah satu keunggulan aplikasi ini. Proses login dibuat sesimpel mungkin dengan berbagai pilihan yang bisa disesuaikan preferensi.

Cara membuat akun baru langsung di aplikasi

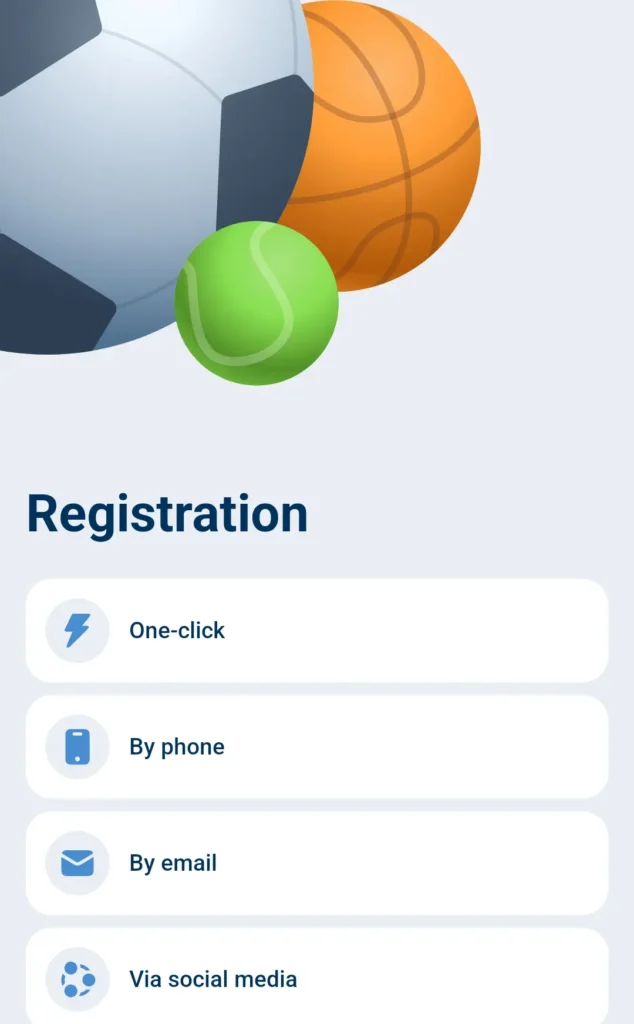

Buka aplikasi yang udah terpasang setelah 1xbet download, terus cari tombol “Daftar” yang ada di halaman depan. Gampang banget nemunya!

Nih, 1xBet apps kasih beberapa pilihan cara daftar yang praktis:

- One-Click: Yang paling cepat! Cuma pilih negara & mata uang (IDR), trus sistem langsung kasih username dan password secara otomatis

- Email: Ini yang paling lengkap. Kamu perlu isi nama lengkap, tanggal lahir, dan email aktif. Jangan lupa bikin password yang kuat-campuran huruf besar-kecil plus angka ya

Mana yang mau kamu pilih? Tinggal klik aja sesuai preferensimu!

Opsi login cepat: One-click, nomor ponsel, atau email

Bingung mau login yang gimana? Tenang, pilihannya lengkap, bisa pake satu klik, nomor HP, atau email. Pilih yang paling nyaman aja buat kamu!

Nih, biar kamu makin paham:

- One-Click Login: Ini nih yang paling ce-pat! Tapi cuma buat kamu yang sebelumnya udah pernah login di perangkat yang sama

- Login Pake Nomor HP: Tinggal masukin nomor, terus isi kode verifikasi dari SMS, langsung masuk

- Login dengan Email: Opsi yang paling standar dan banyak dipake

Saran, pilih cara yang paling gampang kamu inget. Biar nggak ribet nyari-nyari password terus!

Verifikasi identitas dan keamanan akun pengguna

Nah, soal verifikasi akun nih, jangan dianggap remeh, ya! Proses ini wajib kamu lewatin sebelum narik dana pertama kali. Caranya gampang banget, kok. Kamu tinggal upload foto KTP atau kartu identitas lain yang masih berlaku langsung dari menu profil.

Biasanya proses ini butuh waktu 1 sampai 3 hari kerja. Keuntungannya, akun yang udah terverifikasi bakal punya limit penarikan yang lebih gede dan bisa akses semua fitur tanpa batasan.

Buat keamanan ekstra, jangan lupa aktifin two-factor authentication (2FA). Dan yang paling penting, jangan pernah bagiin data login ke orang lain.

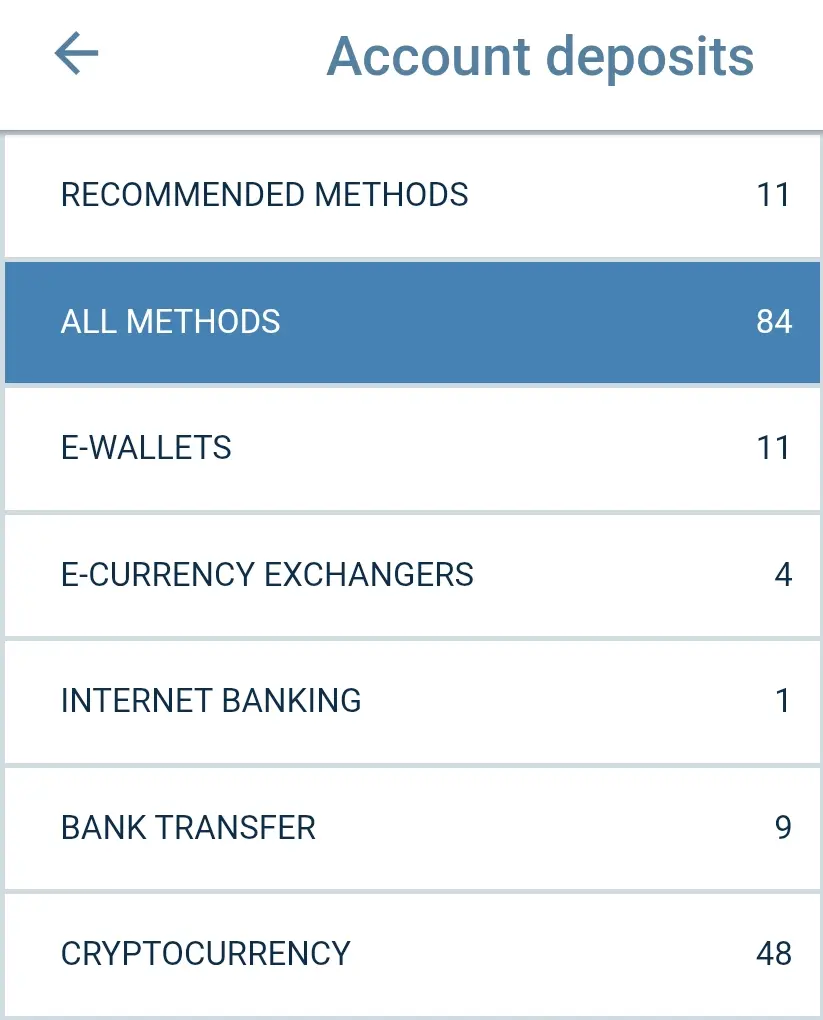

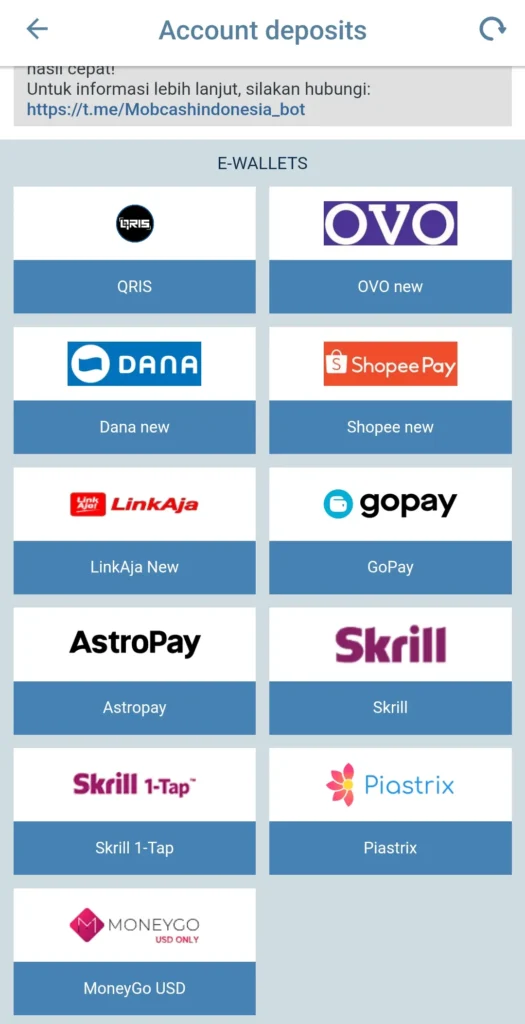

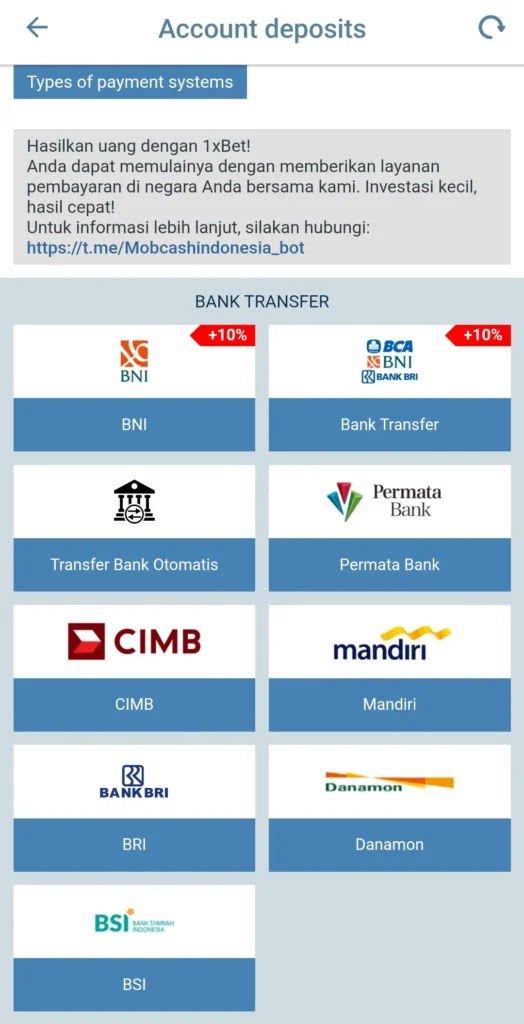

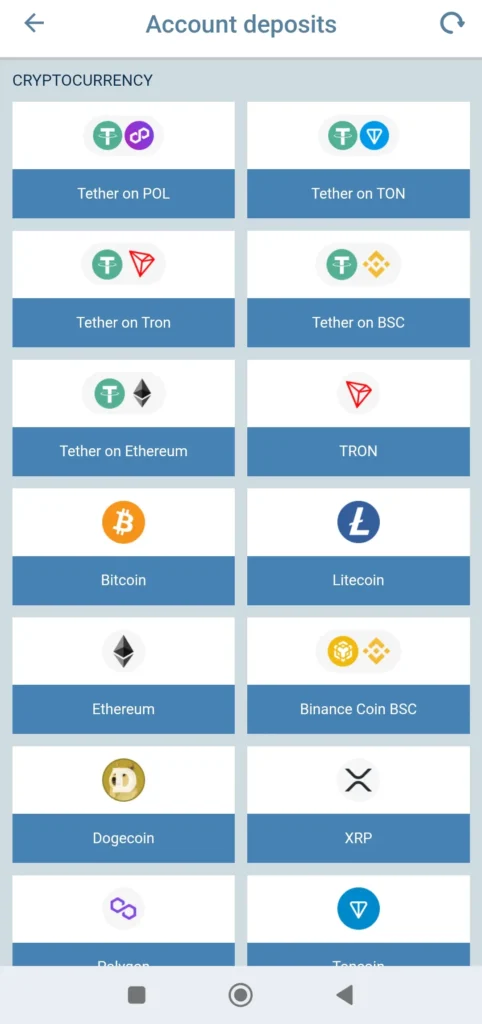

Cara Deposit dan Penarikan Uang di 1xBet Application

Metode pembayaran lokal Indonesia (bank, e-wallet, pulsa)

Bingung mau pilih metode bayar yang mana? Santai aja, aplikasi ini punya banyak opsi! Mulai dari e-wallet, transfer bank, sampai pembayaran digital lainnya tersedia lengkap.

Yang penting, perhatiin baik-baik nominal minimal dan maksimalnya biar transaksi kamu nggak gagal. Percuma kan udah buru-buru 1xbet download tapi salah masukin jumlah deposit?

Dengan banyaknya pilihan yang ada, pasti ada yang cocok dengan gaya transaksi kamu.

Minimal deposit dan waktu proses transaksi

Buat yang mau isi saldo, tenang aja! Deposit mulai dari Rp 10.000 doang.

Pilihannya juga lengkap banget:

- E-wallet: Dukungan untuk banyak provider, proses cepat

- Transfer bank: Bisa pake bank lokal Indonesia

- Cryptocurrency: Tersedia puluhan koin

Tips menghindari error saat melakukan deposit atau withdraw

Biar transaksi selalu lancar, perhatikan hal-hal sederhana ini. Pertama, pastikan nama di akunmu sama persis dengan nama pemilik rekening bank atau e-wallet.

Nih tips lainnya buat kamu yang baru selesai 1xBet download app:

- Screenshot bukti transfernya dan simpan sampai dana masuk.

- Jangan pernah kirim duit dari akun orang lain.

- Kalau dananya nggak masuk, hubungi customer service.

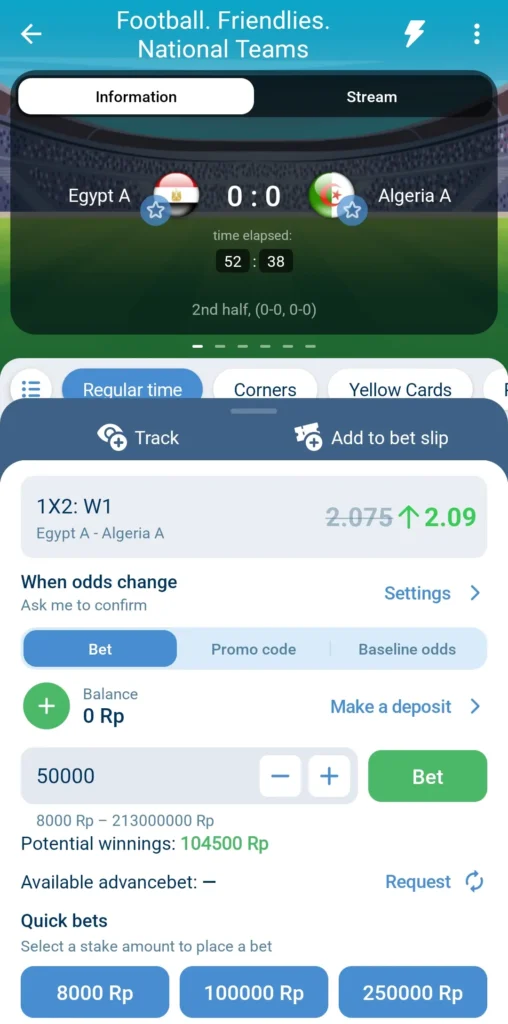

Cara Taruhan Menggunakan 1xBet App

Langkah memasang taruhan olahraga dari mobile app

Gimana sih cara pasang taruhan olahraga yang bener? Gampang banget, kok! Pertama, buka aplikasi dan login pake akun yang udah kamu daftarin. Abis itu, langsung aja pilih menu “Sport” yang ada di halaman depannya.

Nah, sekarang tinggal cari pertandingan yang kamu mau. Kamu bisa jelajahi kategori olahraga satu per satu atau langsung search aja namanya.

Sekarang pilih jenis taruhannya dan klik odds yang diinginkan. Jangan lupa isi jumlah taruhan dan konfirmasi.

Gampang kan? Makanya buruan 1xbet download dan coba sendiri pengalamannya.

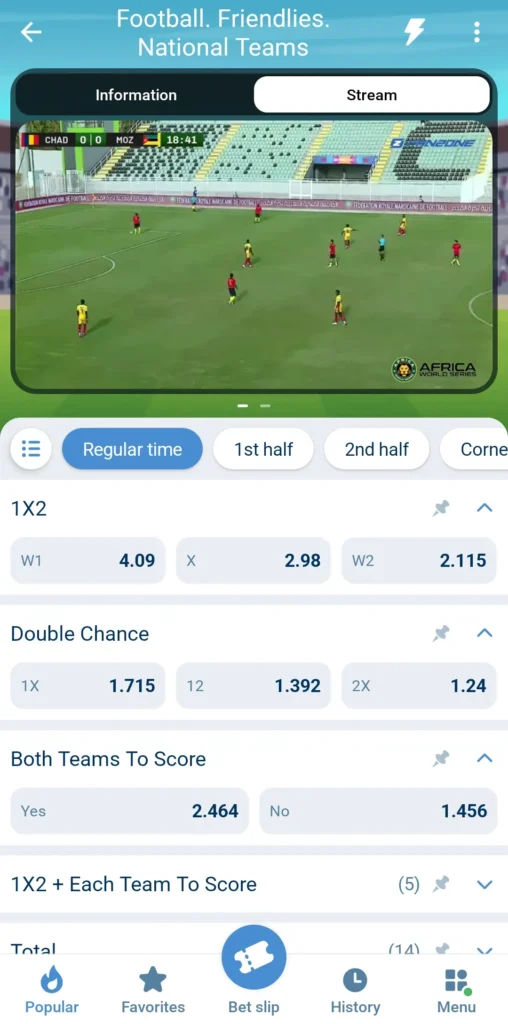

Live betting & streaming langsung di 1xBet apps

Serunya pasang taruhan sambil liat pertandingan langsung! Fitur live betting bikin kamu bisa taruhan saat game berlangsung.

Buat pertandingan besar, kamu juga bisa nonton streaming langsung tanpa pindah aplikasi. Semua ini tersedia dalam satu 1xbet apk yang sudah terpasang.

Fitur keren lainnya:

- Statistik pertandingan update real-time, bantu kamu analisis dengan cepat.

- Ada opsi cash out, jadi kamu bisa tarik dana kemenangan sebelum pertandingan selesai. Pas banget kalau kamu udah puas sama hasil yang didapat!

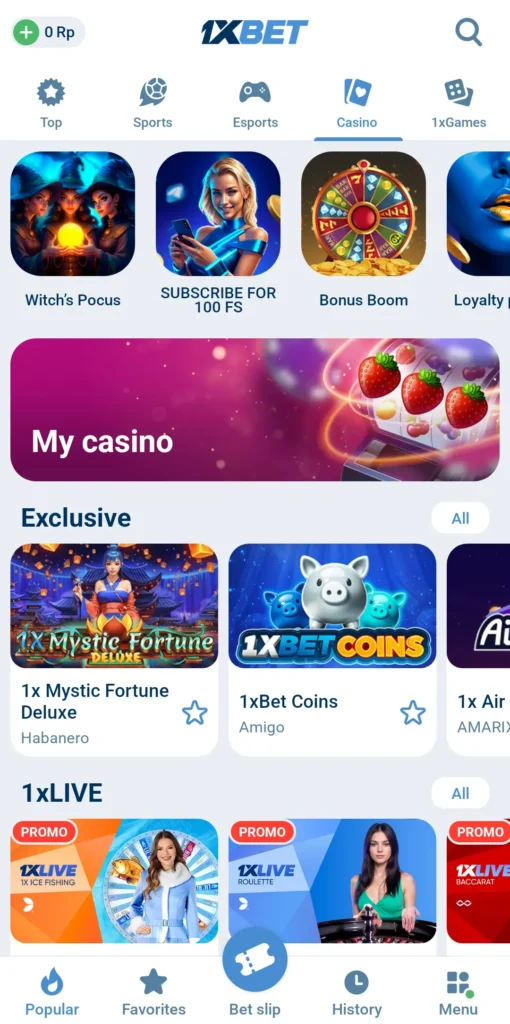

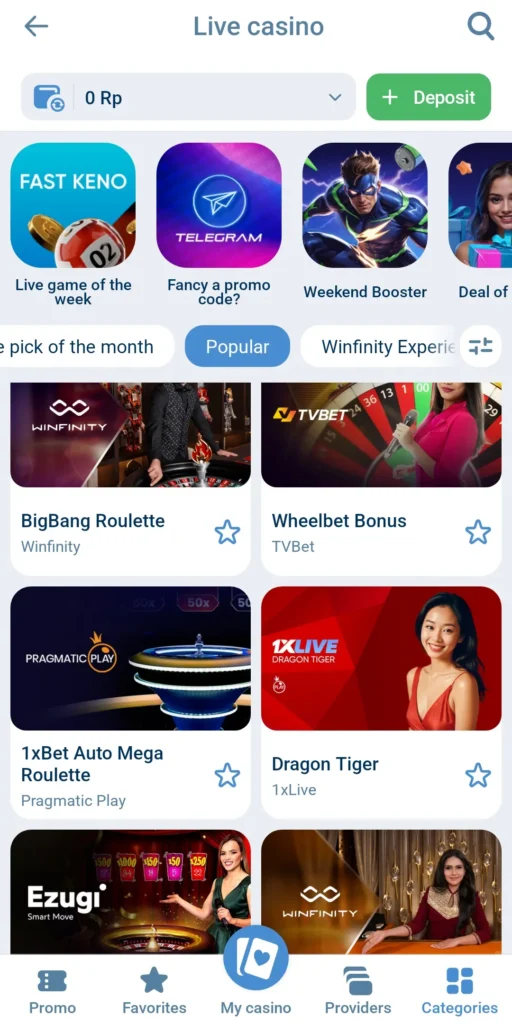

Cara bermain game kasino & slot di aplikasi 1xBet

Mau main casino langsung dari HP? Gampang banget! Begitu buka 1xBet app, langsung aja klik menu “Casino” yang ada di halaman depan. Di sana udah nunggu ratusan slot seru dari provider top kayak Pragmatic Play, Habanero, sama Microgaming.

Pusing milihnya? Pakai aja fitur filter biar cepet nemu game favorit. Kalau pengen merasakan sensasi kayak di casino beneran, buka aja tab “Live Casino”. Permainan kayak Baccarat, Blackjack, Roulette, dan Sic Bo paling laris di antara pemain Indonesia.

Coba dulu kalau ragu! Banyak game yang punya mode demo, jadi bisa dicoba tanpa pakai uang asli. Tapi kalau udah yakin, jangan lupa cek dulu saldomu cukup apa nggak. Selamat bermain!